Why Anyone with an Interest in Farmland Should Be Paying Attention to the USDA Crop Report and the Commodity Market

USDA’s latest crop report released Tuesday January 12th held a surprise, confirmed a trend, and maybe cemented a longer-term shift in farm commodity prices when placed in context with other market information.

The surprise, at least for traders and market watchers, was a larger than expected downward adjustment in the estimated 2020 corn yield. The reduction of 3.8 bushels from December estimate of 175.8 to updated figure of 172 bushels per acre may not sound like much but is the largest since about mid-way through Bill Clinton’s first term. Consequently, nearby corn futures closed the day limit up reaching over $5.30, the highest price since 2013.

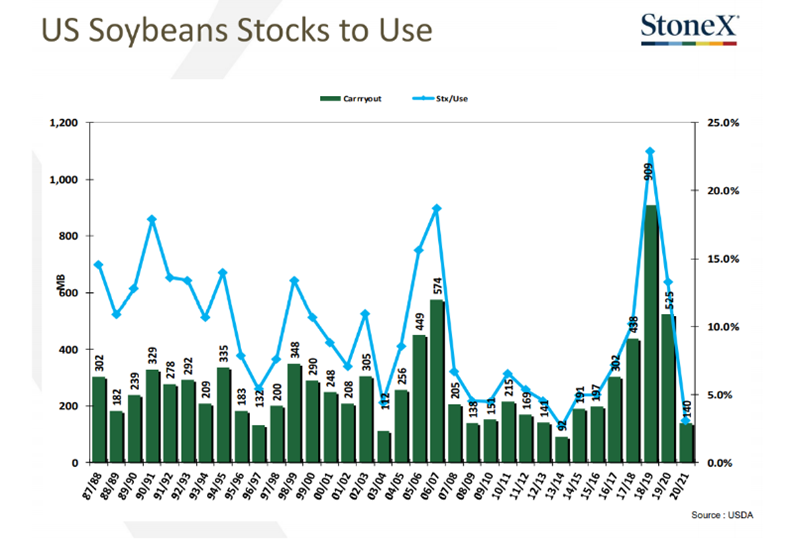

The confirmed trend is tightening soy supplies. Although the 2020 U.S. crop is 583 million bushels (16%) larger than 2020, the estimated end of crop year stocks to use ratio has dropped from a comfortable 13.3% last year to a barely pipeline filling 3.1%, the lowest since the 2013/14 crop year. January soybeans jumped 25½¢, closing at $14.36½ per bushel, the highest since June 2014.

So why could this be a longer-term shift in prices, or more precisely, an upward price cycle adjustment that lasts more than a season or just until planting? The underlying context in which to place the surprise corn yield drop is the primary driver of reduced soy supply: much higher exports to China.

China has a perfect storm for increased prices, the first being a drought last summer which significantly reduced yields. Additionally, Chinese hog production is reportedly back to about 80% of the pre-African Swine Fever which reduced the world’s largest national herd by more than 50%. Additionally, because the use of food waste as feed has been banned due to its possible role in spreading the disease, soymeal use is already back up to pre disease levels even though there is a long way to go in rebuilding the herd. To sum up, China is short of corn and soy at a time when their demand will continue to increase.

The final piece of context is that this is all coming to pass at time during which South America is experiencing a La Nina induced drought during the heart of its growing season. Which means its forthcoming harvest will not be sufficient fully re-stock the system.

And neither is the U.S. likely to rebuild enough stocks in 2021 to put grains back into surplus. We’re starting from too low a base at a time of increasing demand. I’ll save that explanation for the next post. To sum things up for now, we appear to be in a commodity market shift likely to last at least one year and more likely at least two to three. That should be supportive of farm ground values and leases just as it was from 2010 – 2014

Acknowledgement: Charts watermarked as StoneX curtesy of the fantastic analytics team at StoneX Group, with a particular hat tip to Arlan Sunderman and his always insightful Market Outlook. If you have an interest in the nuts and bolts in commodities markets, you should be following him. https://my.stonex.com/s/author?language=en_US&authorId=3636